-

Articles + –

Amazons healthcare reach grows as Insurtech and senior innovations are on the horizon

For the health insurance and pharmaceutical industries, 2017 was the year to watch Amazon. Over the course of 12 months, the ecommerce titan rolled out a series of quiet, but bold moves:

- In April 2017, Amazon Japan partnered with two pharmacy chains, Cocokara Fine Inc. and Matsumotokiyoshi Holdings Co., in a deal to launch a service offering same-day delivery of pharmacy items such as cosmetics and medicine. As a part of this service, Amazon.co.jp began selling category No. 1 drugs on its website. These drugs require consultation with a pharmacist before purchase.

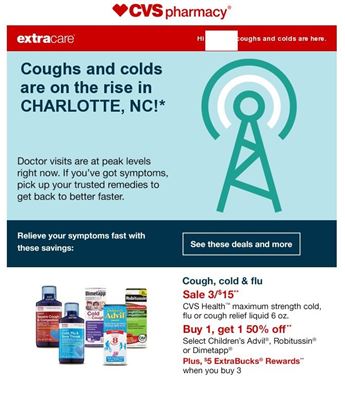

- In August 2017, with little fanfare, Amazon debuted “Basic Care,” an exclusive, private-label line of 60 over-the-counter healthcare products. While this strategic choice has the potential to add significant profits to the company’s bottom line, tenured pharmacy retailers like CVS and Walgreens are undoubtedly less thrilled as they will likely suffer from diminished market share. Although these companies rely most heavily on prescription sales, OTC medications and overall consumer wellness is central to the identity of both brands. (In the marketing images from CVS and Walgreens below, you can see how they market the value and quality of their OTC brands.) Currently, OTC medications play a significant role in consumer health practices. In fact, Mintel’s US report on health management shows that 44% of US consumers say they take an OTC medication on a daily or weekly basis.

- Signaling an interest in the US pharmaceutical space, Amazon obtained wholesale pharmacy licenses in at least 12 US states. These applications were filed discretely and throughout the year.

To date, reports of Amazon’s expanding healthcare interest has plagued industry leaders with wild stock fluctuations, concerns of disruption and, most gravely, the threat of insurmountable competition. While there are many market forces to account for—and Amazon is only one variable—late 2017 and early 2018 saw a record number of subsequent health care industry mergers, acquisitions and partnerships. For example, in a $69 billion deal, CVS announced it would purchase health insurer Aetna. Meanwhile, Cigna recently reported that it would buy Express Scripts, the nation’s largest pharmacy benefit manger, for $52 billion. It appears that health insurers and pharmaceutical retailers are joining forces to remain competitive amid a roiling healthcare landscape.

But was 2017 just the beginning? As we close out the first quarter of 2018, it is clear the answer is a resounding yes. Let’s take a look at a sample of Amazon headlines from the past three months:

- In early January, it was announced that Amazon was investing $15.7 million in Indian insurtech Acko, which provides online-only insurance products. Under the deal, Amazon’s Indian business will reportedly act as Acko’s distributor, and co-develop new insurance products with the company.

- In late January, Amazon formed an independent company with Berkshire Hathaway and JPMorgan Chase to independently explore and develop healthcare coverage innovations.

Most recently, in March 2018, CNBC reported that Amazon is collaborating with AARP to share research and design technology for aging populations with a focus on unmet healthcare needs and social isolation. Just as health insurers see Medicare plans (and the older adults who receive those benefits) as the cornerstone of their future success, consumer technology companies like Amazon, Apple and Alphabet see meeting the needs of aging Baby Boomers as key to retaining market dominance. According to Mintel research on lifestyles of US seniors, more than three out of four seniors say that their health is one of their current priorities, and more than half are looking to improve their health over the next five years. As these influential companies pool resources and develop new products together, the healthcare industry could potentially see a fundamental transformation.

Most recently, in March 2018, CNBC reported that Amazon is collaborating with AARP to share research and design technology for aging populations with a focus on unmet healthcare needs and social isolation. Just as health insurers see Medicare plans (and the older adults who receive those benefits) as the cornerstone of their future success, consumer technology companies like Amazon, Apple and Alphabet see meeting the needs of aging Baby Boomers as key to retaining market dominance. According to Mintel research on lifestyles of US seniors, more than three out of four seniors say that their health is one of their current priorities, and more than half are looking to improve their health over the next five years. As these influential companies pool resources and develop new products together, the healthcare industry could potentially see a fundamental transformation.

Most recently, in March 2018, CNBC reported that Amazon is collaborating with AARP to share research and design technology for aging populations with a focus on unmet healthcare needs and social isolation. Just as health insurers see Medicare plans (and the older adults who receive those benefits) as the cornerstone of their future success, consumer technology companies like Amazon, Apple and Alphabet see meeting the needs of aging Baby Boomers as key to retaining market dominance. According to

Most recently, in March 2018, CNBC reported that Amazon is collaborating with AARP to share research and design technology for aging populations with a focus on unmet healthcare needs and social isolation. Just as health insurers see Medicare plans (and the older adults who receive those benefits) as the cornerstone of their future success, consumer technology companies like Amazon, Apple and Alphabet see meeting the needs of aging Baby Boomers as key to retaining market dominance. According to What we think

Was the pharmacy partnership in Japan a trial balloon for bigger markets such as the US and abroad? What about its investment in an Indian insurtech and its work with AARP? Both of these companies sell insurance products (like in the image above, AARP licenses its brand through a longstanding relationship with UnitedHealth Group), but to radically different consumers. Amazon has been making moves in the healthcare space for over 17 months with direction that was unclear. Until now.

On June 28th, Amazon announced it was acquiring the online pharmacy company, PillPack. As Walgreens Boots Alliance CEO Stefano Pessina aptly noted, “Yes, it’s a declaration of intent from Amazon.” To date, the company has been coy about its ultimate healthcare ambitions. Through the acquisition of PillPack, Amazon takes an irrevocable step that threatens to eliminate one of the few distinguishing features pharmacy chains have used to fend off the e-commerce titan, the sale of prescription drugs.

With companies like Sears and Toys ‘R Us to serve as cautionary tales, retail pharmacies and associated health insurers will soon find their high-profit cash business facing intense competition. Consumers and businesses alike should expect a mass marketplace shakeout over the course of the next few years. As companies like CVS and Walgreens plan their critical next steps, the goal cannot simply be to survive. While this is Amazon’s first big move in healthcare, it will almost surely not be its last.

Caitlin Moling is Mintel Comperemedia’s Director of Insights, Insurance, focused on consumer and industry trends and competitive intelligence for insurance clients.

-

Mintel StoreGet smart fast with our exclusive market research reports, delivering the latest data, innovation, trends and strategic recommendations....View reports

Mintel StoreGet smart fast with our exclusive market research reports, delivering the latest data, innovation, trends and strategic recommendations....View reports -

Mintel LeapMintel Leap is a revolutionary new AI-powered platform that will transform your research process....Book a demo

Mintel LeapMintel Leap is a revolutionary new AI-powered platform that will transform your research process....Book a demo

-

Mintel’s Most Innovative Beauty, Personal Care and Household 2024Beauty and Personal CareDownload

A celebration of innovation and the very best of new beauty, personal care and household product development.Download

A celebration of innovation and the very best of new beauty, personal care and household product development.Download -

Mintel’s Most Innovative Food and Drink 2024Food and DrinkDownload

A celebration of innovation and the very best of new food and drink product development.Download

A celebration of innovation and the very best of new food and drink product development.Download -

2024 Global Consumer TrendsConsumer ResearchDownload

Identifies five consumer behaviour trends that will shape consumer markets in 2024 and beyond.Download

Identifies five consumer behaviour trends that will shape consumer markets in 2024 and beyond.Download -

2024 Global Food and Drink TrendsFood and DrinkDownload

Identifies three consumer behaviour trends that will shape food and drink markets in 2024 and beyond.Download

Identifies three consumer behaviour trends that will shape food and drink markets in 2024 and beyond.Download -

2024 Global Beauty and Personal Care TrendsBeauty and Personal CareDownload

Identifies three consumer behaviour trends that will shape beauty and personal care markets in 2024 and beyond.Download

Identifies three consumer behaviour trends that will shape beauty and personal care markets in 2024 and beyond.Download -

2024 Omnichannel Marketing TrendsAdvertising and MarketingDownload

Learn how marketers can break through the noise with revitalized marketing strategies that call on pre-digital tactics, disrupt linear funnel thinking, and demonstrate a true commitment to action.Download

Learn how marketers can break through the noise with revitalized marketing strategies that call on pre-digital tactics, disrupt linear funnel thinking, and demonstrate a true commitment to action.Download -

2024 Telecom & Media Marketing TrendsAdvertising and MarketingDownload

Learn how telecom and media brands will continuously challenge barriers to entry, recontextualize nostalgia, and emphasize consumer customization.Download

Learn how telecom and media brands will continuously challenge barriers to entry, recontextualize nostalgia, and emphasize consumer customization.Download -

2024 Financial Services Marketing TrendsFinancial ServicesDownload

Learn how financial services brands are changing their messaging and product strategies to prioritize consumer-centric value, seamless experiences, and the preferences of younger generations.Download

Learn how financial services brands are changing their messaging and product strategies to prioritize consumer-centric value, seamless experiences, and the preferences of younger generations.Download