Only those living underground would have not heard the name of the teen pop sensation Taylor Swift over the past few years. Recently it was announced that her latest album, 1989, broke records for the biggest sales week since 2002, as she sold nearly 1.3 million copies in the first week of sales. In conjunction with the release, she announced her withdrawal from one of the biggest online music services, Spotify.

Looking at the music market as a whole, the value of UK music sales picked up for the first time since 2011 last year, with sales reaching £730 million, a 2% increase on the year before. Sales in 2014 are still seeing growth, with a 1.5% growth to reach £741 million. Focusing more specifically on album sales, physical albums have struggled between 2012 and 2013, falling 6% from 367 million in 2013 to 344 million in 2014. Online album sales, in contrast, are going from strength to strength, rising 20% between 2012 and 2013 from £134 million to £161 million.

Samuel Gee, Senior Technology Analyst, takes a look at the role of streaming services in the music industry in the UK and what Swift’s exit from Spotify says about the state of the market.

Taylor Swift’s withdrawal from Spotify was unexpected, coming hot on the heels of her record breaking sales. In an interview shortly afterward, she clarified that she wasn’t willing to dedicate her life’s work to a “grand experiment”, as she called the streaming service.

Behind the rhetoric of her statement is a reiteration of the view expressed by, amongst others, Thom Yorke, Bob Dylan and Metallica; that Spotify doesn’t sufficiently remunerate artists for their work. This is the real division between content producers (like Swift) and distributors (like Spotify).

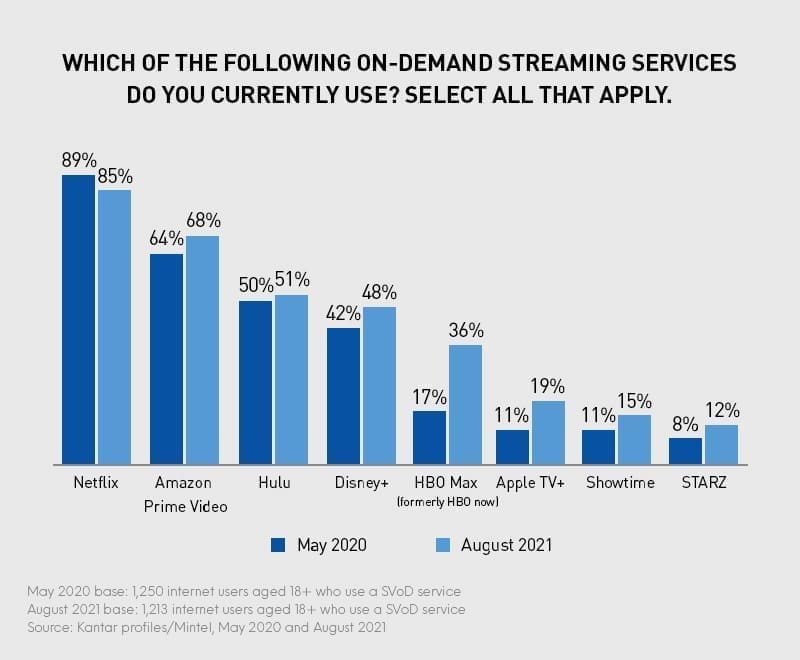

The broader question of whether digital distribution streaming services are legitimate, profitable and stable has long since been answered. Spotify, Netflix, Kindle Unlimited, EA Access and more have demonstrated that there is an enormous consumer market for the unlimited consumption of content in exchange for monthly payments.

There also seems to be proof that the provisions of these services tend to cut down on piracy. Digitally native 16-24s – aware that the web facilitates the immediate sharing and dissemination of content on a global scale – have long since lost patience with legacy distribution windows and territorial restrictions on content. Adoption of streaming alternatives has provided them with a robust alternative to simply taking content that remains available elsewhere.

Plaguing Swift, though, will be a concern that despite the massive consumer demand, the services dilute the value and power of the content creators – power already much reduced after the music industry’s lead-footed response to the digital revolution of the early 2000’s.

She may not have a choice though. Streaming subscription services are already firmly part of the consumer lexicon. Just as ten years ago refusing to release a CD would have been an impossibility, in the years to come, abstaining from participation in streaming services may not be a viable choice.

For more information on Mintel’s Music and Video Purchasing report click here.