-

Articles + –

Market Barometer Issue 50 – Tyres – Rolling on

This month’s Market Review looks at at the tyre market; which quickly recovered from the recession at the end of the last decade.

Source: Mintel Global Market Sizes

An economic indicator?

There is some logic in believing tyre sales reflect world economic health. The OEM (Original Equipment Manufacturer) segment is an indication of the might of automotive manufacturing in any nation; while the replacement sector is a measure of the amount of movement, and thereby trade, on the transport system.

A bounce back

In 2008 when the financial rumblings started to reverberate around the globe, tyre sales had already started to slide and, in the 20 largest economies, they fell by 1%. The following year, when the recession was really beginning to bite, there was a further 4% reduction. However, in 2010 the market had more than recovered lost ground by expanding by twice the rate of the previous year’s contraction. Since then, the market has been steadier but in a gradually upward direction.

China power

It is a few years yet before China becomes the world largest economy but, in tyres, it has already long been there. This is in part due to the growing number of vehicles on the road, both for the growing number of affluent, car-driving consumers, but also for the commercial vehicles delivering goods to the stores and transporting manufactures to the ports for exporting. However, the other side to demand has been the burgeoning Chinese automotive industry, where the number of cars and light vehicles leaving the production line in 2013 was due to surpass that of Europe.

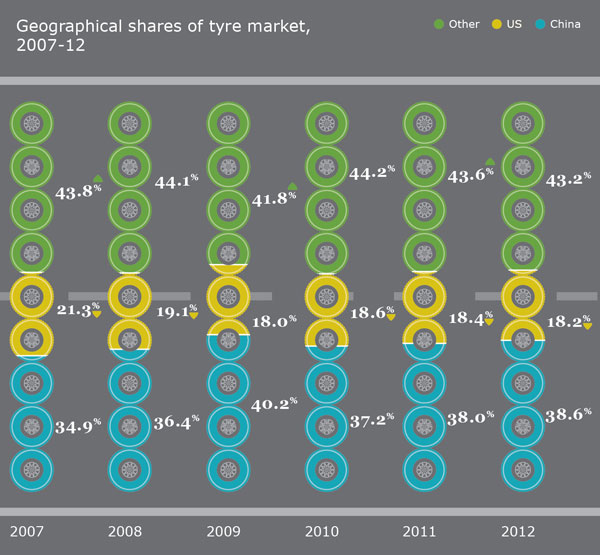

Continually turning

China’s share of world sales shown in the graphic has largely been at the expense of the US. It has been rising in recent years but has not reached the peak of 2009 which was largely a reflection of the slump in the West. There are other countries which are beginning to become sizeable target markets. The most noticeable of these are Russia and India which account for 7.4% of world sales compared with 5.6% five years earlier.

-

Mintel StoreGet smart fast with our exclusive market research reports, delivering the latest data, innovation, trends and strategic recommendations....View reports

Mintel StoreGet smart fast with our exclusive market research reports, delivering the latest data, innovation, trends and strategic recommendations....View reports -

Mintel LeapMintel Leap is a revolutionary new AI-powered platform that will transform your research process....Book a demo

Mintel LeapMintel Leap is a revolutionary new AI-powered platform that will transform your research process....Book a demo

-

Mintel’s Most Innovative Beauty, Personal Care and Household 2024Beauty and Personal CareDownload

A celebration of innovation and the very best of new beauty, personal care and household product development.Download

A celebration of innovation and the very best of new beauty, personal care and household product development.Download -

Mintel’s Most Innovative Food and Drink 2024Food and DrinkDownload A celebration of innovation and the very best of new food and drink product development.Download

-

2024 Global Consumer TrendsConsumer ResearchDownload Identifies five consumer behaviour trends that will shape consumer markets in 2024 and beyond.Download

-

2024 Global Food and Drink TrendsFood and DrinkDownload Identifies three consumer behaviour trends that will shape food and drink markets in 2024 and beyond.Download

-

2024 Global Beauty and Personal Care TrendsBeauty and Personal CareDownload Identifies three consumer behaviour trends that will shape beauty and personal care markets in 2024 and beyond.Download

-

2024 Omnichannel Marketing TrendsAdvertising and MarketingDownload Learn how marketers can break through the noise with revitalized marketing strategies that call on pre-digital tactics, disrupt linear funnel thinking, and demonstrate a true commitment to action.Download

-

2024 Telecom & Media Marketing TrendsAdvertising and MarketingDownload Learn how telecom and media brands will continuously challenge barriers to entry, recontextualize nostalgia, and emphasize consumer customization.Download

-

2024 Financial Services Marketing TrendsFinancial ServicesDownload Learn how financial services brands are changing their messaging and product strategies to prioritize consumer-centric value, seamless experiences, and the preferences of younger generations.Download